Documents

NOTICE OF CONCLUSION OF AUDIT: ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN (AGAR) FOR THE YEAR ENDED 31 MARCH 2021

NOTICE OF CONCLUSION OF AUDIT AND SECTIONS 1,2,3 of the ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN (AGAR) will be found below

Dates for the exercise of public rights 2021

Public rights dates 2021

Audited AGAR for 2024/25

External auditor’s limited assurance opinion 2024/25

On the basis of our review of Sections 1 and 2 of the Annual Governance and Accountability Return, in our opinion the information in Sections

1 and 2 of the Annual Governance and Accountability Return is in accordance with Proper Practices and no other matters have come to our

attention giving cause for concern that relevant legislation and regulatory requirements have not been met.

Please see attached.

Notice of appointment of date for the exercise of public rights

LONGFRAMLINGTON PARISH COUNCIL

|

Notice of appointment of date for the exercise of public rights |

|

Accounts for the year ended 31st March 2025 |

The Local Audit and Accountability Act 2014, and The Accounts and Audit (England) Regulations 2015 (SI 234)

|

1. Date of announcement: 2ND June 2025 |

|

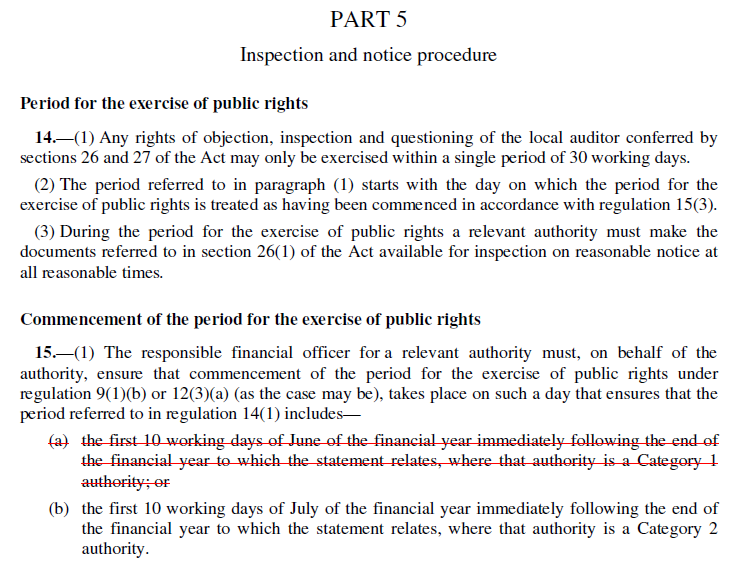

2. Any person interested has the right to inspect and make copies of the accounts to be audited and all books, deeds, contracts, bills, vouchers and receipts relating to them. For the year ended 31 March 2025 these documents will be available on reasonable notice on application to: |

|

Garth Rhodes, Parish Clerk/RFO 5 Wardle Terrace Longframlington Morpeth NE65 8 AB Email: longframlingtonpc@gmail.com Telephone. 01665 570 347

|

|

commencing on 3rd June 2025 |

|

and ending on 14th July 2025 |

|

3. Local Government Electors and their representatives also have: |

|

The auditor can be contacted at the address in paragraph 4 below for this purpose during the inspection period at 2 above. |

Forvis Mazars LLP, The Corner, Bank Chambers, 26 Mosley Street, Newcastle upon Tyne, NE1 1DF Email: local.councils@mazars.co.uk |

|

5. This announcement is made by: GARTH RHODES, PARISH CLERK/RFO

|

Councils’ Accounts: A Summary of Public Rights

The basic position

By law, any interested person has the right to inspect a council’s/meeting’s accounts. If you are entitled and registered to vote in local council elections then you (or your representative) have additional rights to ask the appointed auditor questions about the Council’s accounts or object to an item of account contained within them.

The right to inspect the accounts

When your council has finalised its accounts for the previous financial year it must advertise that they are available for people to inspect. Having given the Council reasonable notice of your intentions, you then have 30 working days to look through the accounting statements in the Annual Return and any supporting documents. By arrangement, you will be able to inspect and make copies of the accounts and the relevant documents. You may have to pay a copying charge.

The right to ask the auditor questions about the accounts

You can only ask the appointed auditor questions about the accounts. The auditor does not have to answer questions about the council’s policies, finances, procedures or anything else not related to the accounts. Your questions must be about the accounts for the financial year just ended. The auditor does not have to say whether they think something the Council has done, or an item in its accounts, is lawful or reasonable.

The right to object to the accounts

If you think that the council has spent money that it should not have, or that someone has caused a loss to the council deliberately or by behaving irresponsibly, you can request the auditor to apply to the courts for a declaration that an item of account is contrary to law. You do this by sending a formal ‘notice of objection’ to the auditor at the address below. The notice must be in writing and copied to the council. In it, you must tell the auditor why you are objecting and what you want the auditor to do about it. The auditor must reach a decision on your objection. If you are not happy with that decision, you can appeal to the courts.

You may also object if you think that there is something in the accounts that the auditor should discuss with the Council or tell the public about in a ‘public interest report’. You must follow the same procedure as outlined in the previous paragraph. The auditor must then decide whether to take any action. The auditor does not have to, but usually will, give reasons for his/her decision and you cannot appeal to the courts. More information is available on the National Audit Office website (see contact details below).

You may not use this ‘right to object’ to make a personal complaint or claim against your council. You should take such complaints to your local Citizens’ Advice Bureau, local Law Centre or your solicitor. You may also be able to approach the Standards Committee of your local principal authority if you believe that a member of the council has broken the Code of Conduct for Members.

What else you can do

Instead of objecting, you can give the auditor information that is relevant to his/her responsibilities. For example, you can simply tell the auditor if you think that something is wrong with the accounts or about waste and inefficiency in the way the Council runs its services. You should make it clear that you are providing information rather than making a formal objection. You do not have to follow any set time limits or procedures. The auditor does not have to give you a detailed report of any subsequent investigation, but will usually tell you the outcome.

A final word

Councils, and so local taxpayers, must meet the costs of dealing with questions and objections. In deciding whether to take your objection forward, one of a series of factors the auditor must take into account is the cost that will be involved. The auditor will only continue with the objection if it is in the public interest to do so. If you appeal to the courts, you might have to pay for the action yourself.

Who should you contact?

For more detailed guidance on electors’ rights and the special powers of auditors, copies of the publication Council Accounts – a guide to your rights are available by calling the National Audit Office on 020 7798 7000 or downloading from the website https://www.nao.org.uk/

If you wish to contact your Council’s appointed external auditor please write to:Gavin Barker, Engagement Lead, Forvis Mazars LLP, local.councils@mazars.co.uk

LONGFRAMLINGTON PARISH COUNCIL: Notice of appointment of date for the exercise of public rights

LONGFRAMLINGTON PARISH COUNCIL

|

Notice of appointment of date for the exercise of public rights |

|

Accounts for the year ended 31st March 2025 |

The Local Audit and Accountability Act 2014, and The Accounts and Audit (England) Regulations 2015 (SI 234)

|

1. Date of announcement: 2ND June 2025 |

|

2. Any person interested has the right to inspect and make copies of the accounts to be audited and all books, deeds, contracts, bills, vouchers and receipts relating to them. For the year ended 31 March 2025 these documents will be available on reasonable notice on application to: |

|

Garth Rhodes, Parish Clerk/RFO 5 Wardle Terrace Longframlington Morpeth NE65 8 AB Email: longframlingtonpc@gmail.com Telephone. 01665 570 347

|

|

commencing on 3rd June 2025 |

|

and ending on 14th July 2025 |

|

3. Local Government Electors and their representatives also have: |

|

The auditor can be contacted at the address in paragraph 4 below for this purpose during the inspection period at 2 above. |

Forvis Mazars LLP, The Corner, Bank Chambers, 26 Mosley Street, Newcastle upon Tyne, NE1 1DF Email: local.councils@mazars.co.uk |

|

5. This announcement is made by: GARTH RHODES, PARISH CLERK/RFO

|

Councils’ Accounts: A Summary of Public Rights

The basic position

By law, any interested person has the right to inspect a council’s/meeting’s accounts. If you are entitled and registered to vote in local council elections then you (or your representative) have additional rights to ask the appointed auditor questions about the Council’s accounts or object to an item of account contained within them.

The right to inspect the accounts

When your council has finalised its accounts for the previous financial year it must advertise that they are available for people to inspect. Having given the Council reasonable notice of your intentions, you then have 30 working days to look through the accounting statements in the Annual Return and any supporting documents. By arrangement, you will be able to inspect and make copies of the accounts and the relevant documents. You may have to pay a copying charge.

The right to ask the auditor questions about the accounts

You can only ask the appointed auditor questions about the accounts. The auditor does not have to answer questions about the council’s policies, finances, procedures or anything else not related to the accounts. Your questions must be about the accounts for the financial year just ended. The auditor does not have to say whether they think something the Council has done, or an item in its accounts, is lawful or reasonable.

The right to object to the accounts

If you think that the council has spent money that it should not have, or that someone has caused a loss to the council deliberately or by behaving irresponsibly, you can request the auditor to apply to the courts for a declaration that an item of account is contrary to law. You do this by sending a formal ‘notice of objection’ to the auditor at the address below. The notice must be in writing and copied to the council. In it, you must tell the auditor why you are objecting and what you want the auditor to do about it. The auditor must reach a decision on your objection. If you are not happy with that decision, you can appeal to the courts.

You may also object if you think that there is something in the accounts that the auditor should discuss with the Council or tell the public about in a ‘public interest report’. You must follow the same procedure as outlined in the previous paragraph. The auditor must then decide whether to take any action. The auditor does not have to, but usually will, give reasons for his/her decision and you cannot appeal to the courts. More information is available on the National Audit Office website (see contact details below).

You may not use this ‘right to object’ to make a personal complaint or claim against your council. You should take such complaints to your local Citizens’ Advice Bureau, local Law Centre or your solicitor. You may also be able to approach the Standards Committee of your local principal authority if you believe that a member of the council has broken the Code of Conduct for Members.

What else you can do

Instead of objecting, you can give the auditor information that is relevant to his/her responsibilities. For example, you can simply tell the auditor if you think that something is wrong with the accounts or about waste and inefficiency in the way the Council runs its services. You should make it clear that you are providing information rather than making a formal objection. You do not have to follow any set time limits or procedures. The auditor does not have to give you a detailed report of any subsequent investigation, but will usually tell you the outcome.

A final word

Councils, and so local taxpayers, must meet the costs of dealing with questions and objections. In deciding whether to take your objection forward, one of a series of factors the auditor must take into account is the cost that will be involved. The auditor will only continue with the objection if it is in the public interest to do so. If you appeal to the courts, you might have to pay for the action yourself.

Who should you contact?

For more detailed guidance on electors’ rights and the special powers of auditors, copies of the publication Council Accounts – a guide to your rights are available by calling the National Audit Office on 020 7798 7000 or downloading from the website https://www.nao.org.uk/

If you wish to contact your Council’s appointed external auditor please write to:Gavin Barker, Engagement Lead, Forvis Mazars LLP, local.councils@mazars.co.uk

ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN (AGAR) FOR THE YEAR ENDED 31st MARCH 2025

ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN (AGAR) FOR THE YEAR ENDED 31st MARCH 2025

Please find below the ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN AGAR FOR THE YEAR ENDED 31st MARCH 2025:

- ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN including the Certificate of Exemption; Annual Internal Audit Report.; Annual Governance Statement; Accounting Statements;

- Analysis of Variances

- Bank Reconciliation

ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN (AGAR) FOR THE YEAR ENDED 31st MARCH 2024

Please find below The NOTICE OF PUBLIC RIGHTS and the ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN AGAR FOR THE YEAR ENDED 31st MARCH 2024:

- Notice of appointment of date of exercise of public rights; Summary of Public Rights

- ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN including the Certificate of Exemption; Annual Internal Audit Report.; Annual Governance Statement; Accounting Statements;

- Analysis of Variances

- Bank Reconciliation

ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN (AGAR) and ACCOUNTS FOR THE YEAR ENDED 31st MARCH 2023

The ANNUAL GOVERNANCE AND ACCOUNTABILITY RETURN ACCOUNTING STATEMENTS FOR THE YEAR ENDED 31st MARCH 2023 ARE AS YET UNAUDITED BY THE EXTERNAL AUDITORS

Please find below the relevant documents related to the AGAR and Annual Accounts 2022/23 :

- Notice of appointment of date of exercise of public rights; Summary of Public Rights; Annual Governance Statement; Accounting Statements; Annual Internal Audit Report.

- Statement of Control

- Summary of Annual Accounts

- Payments & Receipts

- Annual Bank Reconciliation

- Reserves

- Fixed Assets

- Internal Audit Certificate

- Internal Audit Checklist

- Internal Audit Internal Control

1. Public Rights; Annual Governance Statement; Accounting Statements; Annual Internal Audit Report.

1. Public Rights; Annual Governance Statement; Accounting Statements; Annual Internal Audit Report. 2. Statement of Control

2. Statement of Control- 3. Summary of Annual Accounts

- 4.Payments & Receipts

- 5.Annual Bank Reconciliation

- 6. Reserves

- 7. Fixed Assets

- 8. Internal Audit Certificate

- 9. Internal Audit Checklist

- 10. Internal Audit Internal Control